PTC Announces Fourth Fiscal Quarter and Full Year 2023 Results

Solid ARR and Cash Flow in Fourth Fiscal Quarter and Full Year

BOSTON, MA, November 1, 2023 - PTC (NASDAQ: PTC) today reported financial results for its fourth fiscal quarter and full year ended September 30, 2023.

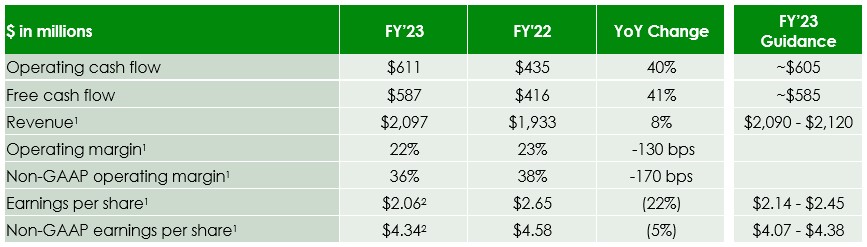

“In our fourth fiscal quarter, we again delivered solid ARR and cash flow results. We reported ARR growth of 26%, organic ARR growth of 15%, and organic constant currency ARR growth of 13%. Our ServiceMax® business contributed an additional 11 points of ARR growth, taking constant currency ARR growth to 23%. Our operating cash flow was $50 million in Q4, up 29% year over year, and $611 million in FY’23, up 40%. Our free cash flow was $44 million in Q4, up 52% year over year, and $587 million in FY’23, up 41%,” said James Heppelmann, CEO, PTC.

“Our differentiated product portfolio and our industry-leading SaaS capabilities align well to the manufacturing industry’s push for digital transformation. On a constant currency basis, Creo and Windchill ARR continued to grow at a double-digit pace, growing 10% and 16% respectively; ServiceMax ended fiscal 2023 at the $170 million of ARR we guided to previously; and our Codebeamer ARR has more than doubled since we acquired the business six quarters ago. Our strong market position and solid execution, coupled with our subscription model, position PTC to continue delivering durable and consistent ARR and cash flow growth,” concluded Heppelmann.

Fourth Quarter and Full Year 2023 Highlights

Key operating and financial highlights are set forth below. The definitions of our operating and non-GAAP financial measures and reconciliations of non-GAAP financial measures to comparable GAAP measures are included below and in the reconciliation tables at the end of this press release.

(1) In Q4’23, revenue growth was 6% year over year on a constant currency basis. Revenue and, as a result, operating margin, operating profit, and earnings per share are impacted by revenue recognition under ASC 606.

(2) In Q4’23, both EPS and non-GAAP EPS were impacted by increased interest expense. Q4’23 EPS included an impact of $0.18 related to a non-cash tax charge.

(3) Q4’23 gross debt includes a deferred acquisition payment related to ServiceMax of $620 million, which was paid in October 2023.

(1) In FY’23, revenue growth was 12% year over year on a constant currency basis. Revenue and, as a result, operating margin, operating profit, and earnings per share are impacted by revenue recognition under ASC 606.

(2) In FY’23, both EPS and non-GAAP EPS were impacted by increased interest expense. FY’23 EPS included an impact of $0.18 related to a non-cash tax charge.

Fiscal 2024 Guidance and Mid-Term Targets

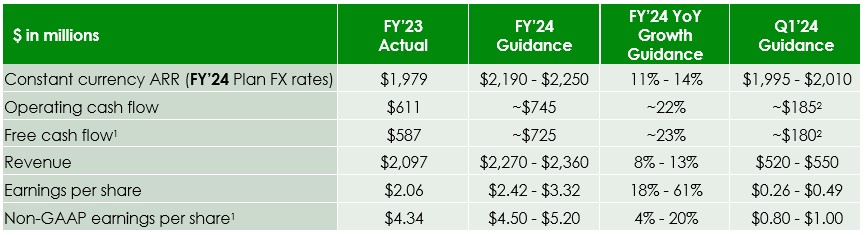

“Despite a challenging backdrop, our financial results in FY’23 were solid, driven by the resilience of our business model, consistent execution, operational discipline, and the actions we have taken to align our investments with our growth opportunities. Our Q4’23 ARR was slightly below the mid-point of our guidance range, as we had lower in-year starts and ended the year with more deferred ARR than we had modeled. At the start of FY’24, deferred ARR with contractually committed start dates over the next 12 months was approximately $20 million higher than at the start of FY’23. Given that, we are raising the low end of our previously communicated ARR growth range and establishing a FY’24 ARR guidance range of 11% to 14%. We continue to expect approximately $725 million of free cash flow in FY’24,” said Kristian Talvitie, CFO, PTC.

Neil Barua, CEO-elect, added, “We continue to target mid-teens growth over the medium term. While the macroeconomic environment could impact any given period, we believe our differentiated product portfolio and market position put us in a good position to drive sustainable top line growth. Given the stability of our subscription license model, we expect non-GAAP operating expense growth at roughly 50% of ARR growth over the medium term, as we continue to invest in our product portfolio. In terms of free cash flow, we are providing targets through FY’26 that represent a three-year CAGR of approximately 20%.”

(1) Refer to the non-GAAP reconciliation table on page 13.

(2) Includes the $30 million imputed interest payment related to the ServiceMax deferred acquisition payment.

(1) Assumes capital expenditures of approximately $25 million.

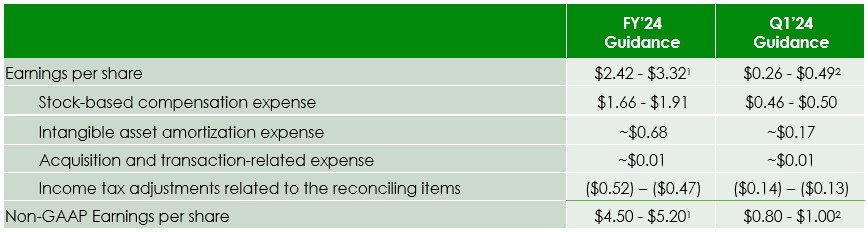

Reconciliation of EPS Guidance to Non-GAAP EPS Guidance

(1) Our FY’24 EPS and non-GAAP EPS guidance are both inclusive of an expected $121 million in interest expense ($96 million, net of tax) or $1.00 per share ($0.80 per share, net of tax). This compares to interest expense in FY’23 of $129 million ($96 million, net of tax) or $1.08 per share ($0.80 per share, net of tax) with the expected decrease in FY’24 primarily due to expected debt paydown during FY’24.

(2) Our Q1’24 EPS and non-GAAP EPS guidance are both inclusive of an expected $36 million in interest expense ($29 million, net of tax) or $0.30 per share ($0.24 per share, net of tax). This compares to interest expense in Q1’23 of $16 million ($14 million, net of tax) or $0.14 per share ($0.12 per share, net of tax) with the expected increase in Q1’24 primarily due to an increase in debt.

FY’24 financial guidance and mid-term targets include the following assumptions:

- We provide ARR guidance on a constant currency basis, using our FY’24 Plan foreign exchange rates (rates as of September 30, 2023) for all periods.

- We expect churn to remain low.

- For cash flow, due to invoicing seasonality, and consistent with the past 3 years, we expect the majority of our collections to occur in the first half of our fiscal year and for fiscal Q4 to be our lowest cash flow generation quarter.

- Compared to FY’23, at the midpoint of FY’24 ARR guidance, FY’24 GAAP operating expenses are expected to increase approximately 3% to 4%, and FY’24 non-GAAP operating expenses are expected to increase approximately 6% to 7%, primarily due to investments to drive future growth and the acquisition of ServiceMax.

- FY’24 GAAP P&L results are expected to include the items below, totaling approximately $283 million to $313 million, as well as their related tax effects:

- approximately $200 million to $230 million of stock-based compensation expense,

- approximately $82 million of intangible asset amortization expense, and

- approximately $1 million of acquisition and transaction-related expense.

- Our FY’24 GAAP and non-GAAP tax rates are expected to be approximately 20%.

- Cash taxes are expected to increase approximately $15 million in FY’24, and approximately $60 million in both FY’25 and FY’26.

- Capital expenditures are expected to be approximately $20 million in FY’24, and approximately $25 million in FY’25 and FY’26.

- Interest payments are expected to be approximately $135 million in FY’24.

- Our long-term goal, assuming our Debt/EBITDA ratio is below 3x, is to return approximately 50% of our free cash flow to shareholders via share repurchases, while also taking into consideration the interest rate environment and strategic opportunities.

- We expect to prioritize paying down our debt in FY’24.

- We expect gross debt of approximately $1.7 billion at the end of FY’24.

- We expect our fully diluted share count to increase by approximately 1 million in FY’24.

PTC’s Fiscal Fourth Quarter and Full Year Results Conference Call

The Company will host a conference call to discuss results at 5:00 pm ET on Wednesday, November 1, 2023. To participate in the live conference call, dial (888) 330-2508 or (240) 789-2735 and provide the passcode 7328695, or log in to the webcast, available on PTC’s Investor Relations website. A replay will also be available.

Important Information About Our Operating and Non-GAAP Financial Measures

Non-GAAP Financial Measures

PTC provides supplemental non-GAAP financial measures to its financial results. We use these non-GAAP financial measures, and we believe that they assist our investors, to make period-to-period comparisons of our operating performance because they provide a view of our operating results without items that are not, in our view, indicative of our operating results. These non-GAAP financial measures should not be construed as an alternative to GAAP results as the items excluded from the non-GAAP financial measures often have a material impact on our operating results, certain of those items are recurring, and others often recur. Management uses, and investors should consider, our non-GAAP financial measures only in conjunction with our GAAP results.

Non-GAAP operating expense, non-GAAP operating margin, non-GAAP gross profit, non-GAAP gross margin, non-GAAP net income and non-GAAP EPS exclude the effect of the following items: stock-based compensation; amortization of acquired intangible assets; acquisition and transaction-related charges included in general and administrative expenses; restructuring and other charges, net; certain non-operating charges and credits; and income tax adjustments. Additional information about the items we exclude from our non-GAAP financial measures and the reasons we exclude them can be found in “Non-GAAP Financial Measures” in our Annual Report on Form 10-K for the fiscal year ended September 30, 2022.

Free Cash Flow: PTC provides information on free cash flow to enable investors to assess our ability to generate cash without incurring additional external financings and to evaluate our performance against our announced long-term goals and intent to return approximately 50% of our free cash flow to shareholders via stock repurchases. Free cash flow is cash provided by (used in) operations net of capital expenditures. Free cash flow is not a measure of cash available for discretionary expenditures.

Constant Currency (CC): We present CC information to provide a framework for assessing how our underlying business performed excluding the effects of foreign currency rate fluctuations. To present CC information, FY’23 and comparative prior period results for entities reporting in currencies other than United States dollars are converted into United States dollars using the foreign exchange rate as of September 30, 2022, rather than the actual exchange rates in effect during that period. All discussion of FY’24 and comparative prior period ARR results (including FY’23 baseline amounts) are reflected using the foreign exchange rates as of September 30, 2023.

Operating Measures

ARR: ARR (Annual Run Rate) represents the annualized value of our portfolio of active subscription software, cloud, SaaS, and support contracts as of the end of the reporting period. We calculate ARR as follows:

- We consider a contract to be active when the product or service contractual term commences (the “start date”) until the right to use the product or service ends (the “expiration date”). Even if the contract with the customer is executed before the start date, the contract will not count toward ARR until the customer right to receive the benefit of the products or services has commenced.

- For contracts that include annual values that increase over time as there are additional deliverables in subsequent periods, which we refer to as ramp contracts, we include in ARR only the annualized value of components of the contract that are considered active as of the date of the ARR calculation. We do not include the future committed increases in the contract value as of the date of the ARR calculation.

- As ARR includes only contracts that are active at the end of the reporting period, ARR does not reflect assumptions or estimates regarding future customer renewals or non-renewals.

- Active contracts are annualized by dividing the total active contract value by the contract duration in days (expiration date minus start date), then multiplying that by 365 days (or 366 days for leap years).

We believe ARR is a valuable operating measure to assess the health of a subscription business because it is aligned with the amount that we invoice the customer on an annual basis. We invoice customers annually for the current year of the contract. A customer with a one-year contract will typically be invoiced for the total value of the contract at the beginning of the contractual term, while a customer with a multi-year contract will be invoiced for each annual period at the beginning of each year of the contract.

ARR increases by the annualized value of active contracts that commence in a reporting period and decreases by the annualized value of contracts that expire in the reporting period.

As ARR is not annualized recurring revenue, it is not calculated based on recognized or unearned revenue and is not affected by variability in the timing of revenue under ASC 606, particularly for on-premises license subscriptions where a substantial portion of the total value of the contract is recognized at a point in time upon the later of when the software is made available, or the subscription term commences.

ARR should be viewed independently of recognized and unearned revenue and is not intended to be combined with, or to replace, either of those items. Investors should consider our ARR operating measure only in conjunction with our GAAP financial results.

Organic Constant Currency ARR: We provide an organic constant currency ARR measure to help investors understand and assess the performance of our business without the distorting effects of ARR from acquisitions in the comparative period and foreign exchange rate fluctuations.

Forward-Looking Statements

Statements in this press release that are not historic facts, including statements about our future financial and growth expectations, guidance, and targets, and potential stock repurchases, are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from those projected. These risks include: the macroeconomic and/or global manufacturing climates may not improve or may deteriorate due to, among other factors, increasing interest rates and inflation, tightening of credit standards and availability, volatile foreign exchange rates, supply chain disruptions, the effects of the Russia/Ukraine conflict, including the effect on energy supplies to Europe, the effects of Mideast tensions and actions, and growing tensions with China, any of which could cause customers to delay or reduce purchases of new software, reduce the number of subscriptions they carry, or delay payments to us, which would adversely affect ARR and/or our financial results, including cash flow; our businesses, including our ServiceMax and SaaS businesses, may not expand and/or generate the ARR and/or cash flow we expect if customers are slower to adopt those technologies than we expect or if they adopt competing technologies; our strategic initiatives and investments, including our accelerated investments in our transition to SaaS and the acquisition of ServiceMax, may not deliver the results when or as we expect; we may be unable to generate sufficient operating cash flow to return 50% of free cash flow to shareholders via share repurchases, and other uses of cash or our credit facility limits could preclude such repurchases; and foreign exchange rates may differ materially from those we expect. In addition, our assumptions concerning our future GAAP and non-GAAP effective income tax rates are based on estimates and other factors that could change, including the geographic mix of our revenue, expenses, and profits. Other risks and uncertainties that could cause actual results to differ materially from those projected are detailed from time to time in reports we file with the Securities and Exchange Commission, including our most recent Annual Report on Form 10-K and Quarterly Reports on Form 10-Q.

About PTC (NASDAQ: PTC)

PTC (NASDAQ: PTC) is a global software company that enables industrial and manufacturing companies to digitally transform how they engineer, manufacture, and service the physical products that the world relies on. Headquartered in Boston, Massachusetts, PTC employs over 7,000 people and supports more than 25,000 customers globally. For more information, please visit www.ptc.com.

PTC Investor Relations Contacts

Matt Shimao

SVP, Investor Relations

[email protected]

[email protected]