PTC Announces Fourth Fiscal Quarter and Full Year 2022 Results

Strong Performance in Fourth Fiscal Quarter and Full Year

BOSTON, MA, November 2, 2022 - PTC (NASDAQ: PTC) today reported financial results for its fourth fiscal quarter and full year ended September 30, 2022.

“In our fourth fiscal quarter, we again delivered strong results. We reported ARR growth of 7%, organic ARR growth of 6%, and organic constant currency growth of 15%. The Codebeamer business, which we acquired in the third quarter, continued to perform well and added an additional point of ARR growth, taking constant currency ARR growth to 16% for the 4th quarter and full year. In fiscal 2022, our cash from operations was $435 million, up 18% year over year, and our free cash flow was $416 million, up 21% year over year. While currency headwinds have impacted our ARR, our solid execution, the timing of our collections, and prudent cost controls have mitigated the impact on cash flow,” said James Heppelmann, President and CEO, PTC.

“Our differentiated product portfolio and industry-leading SaaS capabilities align well to the manufacturing industry’s push for digital transformation. Despite challenging economic conditions, the strong resiliency of our business due to our subscription model and our strong market position, coupled with strong execution, has allowed PTC to surpass all of our key guidance measures throughout fiscal 2022. We are positioned for continued solid performance in fiscal 2023,” concluded Heppelmann.

Fourth Quarter 2022 and Full Year Highlights1

Key operating and financial highlights are set forth below. For additional details, please refer to the Q4’22 earnings presentation and financial data tables that have been posted to the Investor Relations section of our website at investor.ptc.com. Revenue and, as a result, operating margin, operating profit, and earnings per share are impacted by revenue recognition under ASC 606.

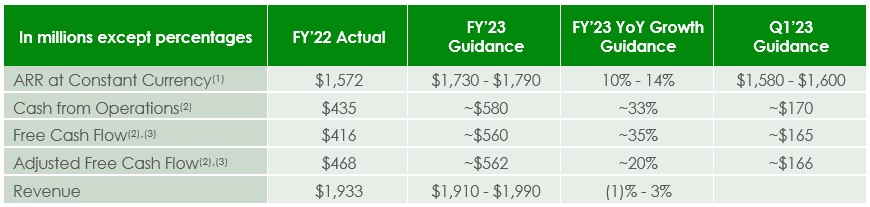

- ARR as reported was $1,572 million at the end of Q4’22, up 7% compared to $1,468 million in Q4’21. On a constant currency basis, Q4’22 ARR was $1,706 million, up 16%, compared to $1,468 million in Q4’21, and exceeded guidance. On an organic basis (excluding Codebeamer, which was acquired in Q3’22), Q4’22 ARR was $1,556 million, up 6% compared to $1,468 million in Q4’21. On an organic constant currency basis, Q4’22 ARR was $1,688 million, up 15% compared to $1,468 million in Q4’21. Foreign exchange rate fluctuations had a $134 million negative impact on our Q4’22 reported ARR, compared to our Q4’22 constant currency ARR. ARR at the end of Q4’22 includes a $4 million reduction associated with discontinuing our business operations in Russia in Q2’22.

- Cash flow from operations was $38 million, free cash flow was $29 million, and adjusted free cash flow was $33 million in Q4’22, compared to cash flow from operations of $45 million, free cash flow of $32 million, and adjusted free cash flow of $33 million in Q4’21. For FY’22, cash flow from operations was $435 million, free cash flow was $416 million, and adjusted free cash flow was $468 million, up compared to FY’21 by 18%, 21%, and 20%, respectively. Cash flow results for Q4’22 and FY’22 exceeded guidance. Foreign exchange rate fluctuations had an approximately $30 million negative impact to our FY’22 free cash flow.

- Revenue was $508 million in Q4’22, up 6% compared to $481 million in Q4’21. On a constant currency basis, revenue was up 12% compared to Q4’21. For FY’22, revenue was $1,933 million, up 7% compared to $1,807 million in FY’21, and in-line with guidance. On a constant currency basis, FY’22 revenue was up 11% compared to FY’21. We do not provide constant currency revenue guidance.

- Operating margin was 29% in Q4’22, compared to 24% in Q4’21. Non-GAAP operating margin in Q4’22 was 40%, compared to 37% in Q4’21. For FY’22, operating margin was 23%, compared to 21% in FY’21. Non-GAAP operating margin was 38% in FY’22, compared to 35% in FY’21.

- Earnings per share was $0.90 in Q4’22, compared to $2.46 in Q4’21. Non-GAAP earnings per share in Q4’22 was $1.27, compared to $1.10 in Q4’21. For FY’22, earnings per share was $2.65, compared to $4.03 in FY’21. Non-GAAP earnings per share was $4.58 in FY’22, compared to $3.97 in FY’21. Our Q4’21 and FY’21 GAAP earnings per share benefitted from a $69 million gain on our investment in Matterport, Inc. and a $137 million release of our U.S. valuation allowance.

- Total cash and cash equivalents as of the end of Q4’22 was $272 million. Gross debt was $1.36 billion as of the end of Q4’22. We repaid $75 million on our revolving credit facility in Q4’22. At the end of Q4’21, total cash and equivalents was $327 million and gross debt was $1.45 billion.

- Stock repurchases were $125 million in FY’22.

- 1]The definitions of our operating and non-GAAP financial measures and reconciliations of non-GAAP financial measures to comparable GAAP measures are included below and in the reconciliation tables at the end of this press release.

Fiscal 2023 and Q1’23 Guidance

“PTC delivered solid fourth quarter results. With strong bookings performance and significantly improved churn, we beat our ARR and free cash flow guidance for the quarter and the year. Balancing our momentum and forecast with potential macro uncertainties, we are establishing ARR guidance for fiscal 2023 that represents 10% to 14% constant currency growth over fiscal 2022. We expect revenue, which is significantly impacted by both ASC606 revenue recognition and currency fluctuations, to be approximately flat on a year over year basis. Given the resilience of the business model, our consistent execution, operational discipline and the actions we have taken to align our investments with growth expectations, we expect free cash flow of approximately $560M in fiscal 2023,” said Kristian Talvitie, EVP and CFO, PTC.

“For Q1’23, we are establishing ARR guidance of 14% to 15% constant currency growth compared to Q1’22, and free cash flow guidance of approximately $165 million,” concluded Talvitie.

(1) On a constant currency basis, using our FY’23 Plan foreign exchange rates (rates as of September 30, 2022) for FY’22 actual ARR, FY’23 ARR guidance, and Q1’23 ARR guidance; FY’22 actual ARR at constant currency using our FY’22 Plan foreign exchange rates (rates as of September 30, 2021) was $1,706 million.

(2) FY’23 cash from operations and free cash flow guidance include restructuring payments of approximately $1 million and acquisition and transaction-related payments of approximately $1 million, both of which are excluded from FY’23 adjusted free cash flow guidance; Q1’23 cash from operations and free cash flow guidance include expected restructuring payments of approximately $1 million which is excluded from Q1’23 adjusted free cash flow guidance.

(3) Free cash flow and adjusted free cash flow guidance are net of expected capital expenditures of approximately $20 million in FY’23 and $5 million in Q1’23.

Our FY’23 and Q1’23 financial guidance includes the assumptions below:

- We provide ARR guidance on a constant currency basis, using our FY’23 Plan foreign exchange rates (rates as of September 30, 2022) for all periods.

- We expect FY’23 organic churn to be ~5.5%.

- For cash flow, due to invoicing seasonality, and consistent with the past 2 years, we expect the majority of our collections to occur in the first half of our fiscal year and for Q4’23 to be our lowest cash flow generation quarter.

- At the mid-point of ARR guidance, we expect FY’23 GAAP operating expenses to decrease approximately 4% to 5% and non-GAAP operating expenses to increase approximately 0% to 1% compared to FY’22.

- FY’23 GAAP P&L results are expected to include the items outlined below, totaling $216 million to $231 million, as well as their related tax effects:

- $160 million to $175 million of stock-based compensation expense

- $56 million of intangible asset amortization expense

- Our FY’23 GAAP and non-GAAP tax rate is expected to be approximately 22%.

- Our long-term goal, assuming our Debt/EBITDA ratio is below 3x, is to return approximately 50% of our free cash flow to shareholders via share repurchases, while also taking into consideration the interest rate environment and strategic opportunities.

PTC’s Fiscal Fourth Quarter Results Conference Call

The Company will host a conference call to discuss results at 5:00 pm ET on Wednesday, November 2, 2022. To participate in the live conference call, dial (888) 330-2508 or (240) 789-2735 and provide the passcode 7328695, or log in to the webcast, available on PTC’s Investor Relations website. A replay will also be available.

Important Disclosures

Important Information About Our Non-GAAP Financial Measures

PTC provides supplemental non-GAAP financial measures to its financial results. We use these non-GAAP financial measures, and we believe that they assist our investors, to make period-to-period comparisons of our operating performance because they provide a view of our operating results without items that are not, in our view, indicative of our operating results. These non-GAAP financial measures should not be construed as an alternative to GAAP results as the items excluded from the non-GAAP financial measures often have a material impact on our operating results, certain of those items are recurring, and others often recur. Management uses, and investors should consider, our non-GAAP financial measures only in conjunction with our GAAP results.

Non-GAAP operating expense, non-GAAP operating margin, non-GAAP gross profit, non-GAAP gross margin, non-GAAP net income and non-GAAP EPS exclude the effect of the following items: stock-based compensation; amortization of acquired intangible assets; acquisition and transaction-related charges included in general and administrative expenses; restructuring and other charges, net; certain non-operating charges and credits; and income tax adjustments. Additional information about the items we exclude from our non-GAAP financial measures and the reasons we exclude them can be found in “Non-GAAP Financial Measures” on page 24 of our Annual Report on Form 10-K for the fiscal year ended September 30, 2021.

Free Cash Flow and Adjusted Free Cash Flow: PTC provides information on free cash flow and adjusted free cash flow to enable investors to assess our ability to generate cash without incurring additional external financings and to evaluate our performance against our announced long-term goals and intent to return approximately 50% of our free cash flow to shareholders via stock repurchases. Free cash flow is cash provided by (used in) operations net of capital expenditures. Adjusted free cash flow is free cash flow net of restructuring payments, acquisition and transaction-related payments, and non-ordinary course tax-related payments or receipts. Free cash flow and adjusted free cash flow are not measures of cash available for discretionary expenditures.

Constant Currency (CC): We present CC information to provide a framework for assessing how our underlying business performed excluding the effects of foreign currency rate fluctuations. To present CC information, FY’22 and comparative prior period results for entities reporting in currencies other than United States dollars are converted into United States dollars using the foreign exchange rate as of September 30, 2021, rather than the actual exchange rates in effect during that period. All discussion of FY’23 and comparative prior period ARR results (including FY’22 baseline amounts) are reflected using the foreign exchange rates as of September 30, 2022.

Operating Measures

ARR: We provide an ARR (Annual Run Rate) operating measure to help investors understand and assess the performance of our business as a SaaS and on-premises subscription company. ARR represents the annualized value of our portfolio of active subscription software, cloud, SaaS, and support contracts as of the end of the reporting period.

We believe ARR is a valuable operating metric to measure the health of a subscription business because it captures expected subscription and support cash generation from customers.

Organic Constant Currency ARR: We provide an organic constant currency ARR measure to help investors understand and assess the performance of our business without the effect of ARR (other than insignificant amounts) from acquisitions in the comparative period and foreign exchange rate fluctuations.

Because our ARR measures represent the annualized value of customer contracts as of a point in time, they do not represent revenue for any particular period or remaining revenue that will be recognized in future periods.

Churn: We provide churn measures to enable investors to understand and assess our customer contract retention. Churn represents the difference between the ARR amount for all subscription software, cloud, SaaS, and support contracts ended within a reporting period and the annualized renewal transactions started within a reporting period, as of the end of the reporting period.

Forward-Looking Statements

Statements in this press release that are not historic facts, including statements about our future financial and growth expectations and targets, and potential stock repurchases, are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from those projected. These risks include: the macroeconomic and/or global manufacturing climates may not improve when or as we expect, or may deteriorate, due to, among other factors, the effects of the COVID-19 pandemic, including supply chain disruptions, increasing interest rates and inflation, volatile foreign exchange rates and the current strength of the U.S. dollar, and the effects of the Russia/Ukraine conflict, including the effect on energy supplies to Europe, which could cause customers to delay or reduce purchases of new software, reduce the number of subscriptions they carry, or delay payments to us, all of which would adversely affect ARR and our financial results, including cash flow; our businesses, including our SaaS businesses, may not expand and/or generate the revenue or ARR we expect if customers are slower to adopt our technologies than we expect or if they adopt competing technologies; our strategic initiatives and investments, including our accelerated investments in our transition to SaaS, may not deliver the results when or as we expect; we may be unable to generate sufficient operating cash flow to return 50% of free cash flow to shareholders, and other uses of cash or our credit facility limits or other matters could preclude such repurchases; and foreign exchange rates may differ materially from those we expect. In addition, our assumptions concerning our future GAAP and non-GAAP effective income tax rates are based on estimates and other factors that could change, including the geographic mix of our revenue, expenses, and profits. Other risks and uncertainties that could cause actual results to differ materially from those projected are detailed from time to time in reports we file with the Securities and Exchange Commission, including our most recent Annual Report on Form 10-K and Quarterly Reports on Form 10-Q.

About PTC (NASDAQ: PTC)

PTC enables global manufacturers to realize double-digit impact with software solutions that enable them to accelerate product and service innovation, improve operational efficiency, and increase workforce productivity. In combination with an extensive partner network, PTC provides customers flexibility in how its technology can be deployed to drive digital transformation – on premises, in the cloud, or via its pure SaaS platform. At PTC, we don't just imagine a better world, we enable it.

PTC Investor Relations Contacts

Matt Shimao

SVP, Investor Relations

[email protected]

[email protected]

PTC Q4 FY'22 Press Release Tables (PDF)

PTC Q4 FY'22 Earnings Presentation (PDF)