PTC Announces First Quarter FY’17 Results

Strong Start to FY’17 with Bookings and Subscription Bookings Mix Both Exceeding the High End of Guidance

NEEDHAM, MA, January 18, 2017 ‑ PTC (NASDAQ: PTC) today reported financial results for the first quarter ended December 31, 2016.

Overview

First quarter FY’17 GAAP revenue was $286 million; non-GAAP revenue was $287 million. We recorded a GAAP net loss of $9 million or $0.08 per share; non-GAAP net income was $31 million or $0.26 per share.

“Despite foreign currency headwinds, bookings of $90 million and subscription bookings mix of 65% demonstrate a continuation of the momentum we have been building over the past year,” said James Heppelmann, President and CEO, PTC. “In particular, we are very pleased with the first quarter results of our IoT business, which continued to capitalize on our technology and market leadership to deliver bookings well above our expectations. Continued improvements in focus and execution drove solid performance in our Solutions business, led by CAD bookings growth in the double-digits.”

Heppelmann added, “Note that there were significant changes in foreign currencies since we provided guidance in October 2016. Despite these currency headwinds, we are maintaining our FY’17 bookings guidance due to the Q1’17 over performance, and we are reducing revenue and EPS guidance by less than the estimated currency impact.”

Heppelmann continued, “We remain focused on creating significant long-term value for our customers and shareholders through our transition to a subscription business model. It is important to note that a higher subscription mix relative to guidance for the current quarter negatively impacts near-term reported revenue and earnings, as we will record a greater proportion of our revenue on a ratable basis.”

Operating and Financial Overview

Q1’17 operating and financial highlights are set forth below. For additional details, please refer to the prepared remarks and financial data tables that have been posted to the Investor Relations section of our website at investor.ptc.com. Information about our bookings and other reporting measures is provided on page 4.

- Q1’17 license and subscription bookings were $90 million, up 31% YoY, and above the high end of the guidance range of $70 million to $80 million. Changes in foreign currencies, since guidance was provided in October 2016, had a negative $2 million impact on reported bookings. Bookings results were driven by strong performance in IoT, including one IoT mega deal (>$5m in bookings) and one IoT large deal (>$1m in bookings), as well as solid execution within our Solutions business, led by low-teens constant currency bookings growth in CAD.

- Q1’17 subscription annualized contract value (ACV) was $29 million, up 177% YoY and above our guidance range of $19 million to $22 million.

- Q1’17 subscription bookings were 65% of total bookings, above our guidance assumption of 55% and up from 28% in Q1’16. For Q1’17, we estimate that this higher-than-guidance mix of subscription in the quarter, while positive in the long-term, reduced both GAAP and non-GAAP revenue by approximately $9 million and reduced non-GAAP EPS by approximately $0.08 as compared to our guidance, and reduced non-GAAP EPS by approximately $0.27 as compared to Q1’16 subscription mix.

- Strong subscription results contributed to a significant increase in our total deferred revenue – billed plus unbilled, which increased year over year by $248 million, or 43%, to $825 million as of the end of Q1’17.

- Q1’17 GAAP software revenue was approximately $240 million and non-GAAP software revenue was approximately $241 million. These results reflect a higher mix of subscription than last year, and were both down approximately 0.5% year over year and 1% year over year in constant currency. We estimate that the higher mix of subscription than last year reduced both GAAP and non-GAAP Q1’17 software revenue by approximately $34 million or 14%.

- Annualized recurring revenue (ARR) was approximately $819 million for Q1’17, an increase of 9% year-over-year.

- Q1’17 GAAP operating expenses were approximately $200 million; non-GAAP operating expenses were approximately $170 million.

- Q1’17 GAAP operating margin was 2% and non-GAAP operating margin was 15%, which compares to Q1’16 GAAP operating margin of (5%) and non-GAAP operating margin of 21%. We estimate that the higher mix of subscription in Q1’17 reduced non-GAAP operating margin by approximately 260 basis points as compared to guidance mix, and reduced non-GAAP operating margin by approximately 900 basis points as compared to the Q1’16 subscription mix.

- For Q1’17, we recorded a GAAP income tax expense of $3 million, or $0.02 per share; non-GAAP income tax expense was $2 million, or $0.02 per share. The GAAP tax rate for the quarter was (41%) and the non-GAAP tax rate for the quarter was 8%.

- Cash flow used by operations for Q1’17 was ($48) million, and free cash flow was ($55) million, both of which include cash payments for restructuring of $16 million.

- We ended the quarter with total cash, cash equivalents, and marketable securities of $223 million and total debt, net of deferred issuance costs, of $728 million.

Workforce Realignment

In October 2015, reflecting a realignment of resources toward higher growth opportunities and our commitment to operating margin improvement, we announced a plan to repurpose or eliminate approximately 8% of worldwide positions and to consolidate select facilities, which would incur a then expected restructuring charge of $40 million to $50 million. As announced in October 2016, we increased the scope of our realignment, which raised our estimate to approximately $75 million to $80 million (and to approximately 13% of our September 30, 2015 worldwide headcount). As of December 31, 2016, we were materially complete with those actions and had incurred total restructuring charges of approximately $83 million, above the high end of our estimate due to some incremental efficiencies which were identified during the quarter. Of that amount, $37 million was recorded in Q1’16, $5 million in Q2’16, $3 million in Q3’16, $32 million in Q4’16 and $6 million in Q1’17. Substantially all of the charges are attributable to termination benefits.

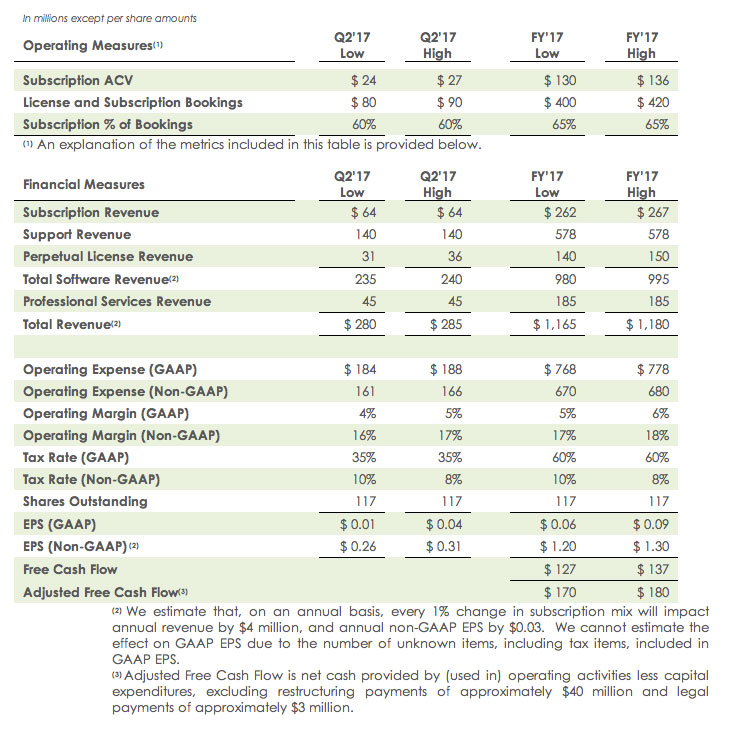

FY’17 Business Outlook

For the second quarter ending April 1, 2017 and for fiscal year 2017, the company expects:

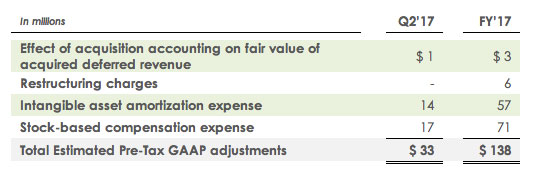

The Q2’17 and full year FY’17 non-GAAP operating margin and non-GAAP EPS guidance exclude the estimated items outlined in the table below, as well as any tax effects and discrete tax items (which are not known or reflected).

PTC’s First Quarter FY’17 Results Conference Call, Prepared Remarks and Financial Data Tables

Prepared remarks for the conference call and financial data tables have been posted to the Investor Relations section of our website at ptc.com. The Company will host a management presentation to discuss results at 5:00 pm ET on Wednesday, January 18, 2017. To access the live webcast, please visit PTC’s Investor Relations website at investor.ptc.com at least 15 minutes before the scheduled start time to download any necessary audio or plug-in software. To participate in the live conference call, dial 800-857-5592 or 773-799-3757 and provide the passcode PTC. The call will be recorded and a replay will be available for 10 days following the call by dialing 866-508-6487 and entering the pass code 3015. The archived webcast will also be available on PTC’s Investor Relations website.

Bookings Metrics

We offer both perpetual and subscription licensing options to our customers, as well as monthly software rentals for certain products. Given the difference in revenue recognition between the sale of a perpetual software license (revenue is recognized at the time of sale) and a subscription (revenue is deferred and recognized ratably over the subscription term), we use bookings for internal planning, forecasting and reporting of new license and cloud services transactions. In order to normalize between perpetual and subscription licenses, we define subscription bookings as the subscription annualized contract value (subscription ACV) of new subscription bookings multiplied by a conversion factor of 2. We arrived at the conversion factor of 2 by considering a number of variables including pricing, support, length of term, and renewal rates. We define subscription ACV as the total value of a new subscription booking divided by the term of the contract (in days) multiplied by 365. If the term of the subscription contract is less than a year, the ACV is equal to the total contract value.

License and subscription bookings equal subscription bookings (as described above) plus perpetual license bookings plus any monthly software rental bookings during the period. Total ACV equals subscription ACV (as described above) plus the annualized value of incremental monthly software rental bookings during the period.

Because subscription bookings is a metric we use to approximate the value of subscription sales if sold as perpetual licenses, it does not represent the actual revenue that will be recognized with respect to subscription sales or that would be recognized if the sales were perpetual licenses, nor does the annualized value of monthly software rental bookings represent the value of any such booking.

Annualized Recurring Revenue (ARR)

We currently offer our solutions on premise, as a cloud service, and as SaaS offerings. Our on-premise solutions can be licensed either as perpetual with annual support contracts or through a subscription, which is a combination of license and support. Beginning in FY’16, we launched a number of initiatives designed to incentivize more of our customers to purchase our solutions on a subscription basis. If successful, these initiatives will cause an increasing percentage of our revenue to come from subscriptions, which is expected to grow our recurring software revenue.

To help investors understand and assess the success of this expected revenue transition, we are providing an Annualized Recurring Revenue operating measure. Annualized Recurring Revenue (ARR) for a given quarter is calculated by dividing the portion of non-GAAP software revenue attributable to subscription and support for the quarter by the number of days in the quarter and multiplying by 365. ARR should be viewed independently of revenue and deferred revenue as it is an operating measure and is not intended to be combined with or to replace either of those items. ARR is not a forecast of future revenue, which can be impacted by contract expiration and renewal rates, and does not include revenue reported as perpetual license or professional services revenue in our consolidated statement of income. Subscription and support revenue and ARR disclosed in a quarter can be impacted by multiple factors, including but not limited to (1) the timing of the start of a contract or a renewal, including the impact of on-time renewals, support win-backs, and support conversions, which may vary by quarter, (2) the ramping of committed monthly payments under a subscription agreement over time, and (3) multiple other contractual factors with the customer including other elements sold with the subscription or support contract, and these elements can result in variability in disclosed ARR.

Navigate Allocation

In FY’16, we launched Navigate, a ThingWorx-based IoT solution for PLM. In FY’17, revenue and bookings for Navigate are being allocated 50% to Solutions and 50% to IoT. FY’16 reported amounts have been reclassified to conform with the current presentation. The impact of the reclassification on FY’16 revenue was immaterial.

Constant Currency Change Metric

Year-over-year changes in revenue and bookings on a constant currency basis compare reported results excluding the effect of any hedging converted into U.S. dollars based on the corresponding prior year’s foreign currency exchange rates to reported results for the comparable prior year period.

Important Information about Non-GAAP References

PTC provides non-GAAP supplemental information to its financial results. We use these non-GAAP measures, and we believe that they assist our investors, to make period-to-period comparisons of our operational performance because they provide a view of our operating results without items that are not, in our view, indicative of our operating results. We believe that these non-GAAP measures help illustrate underlying trends in our business, and we use the measures to establish budgets and operational goals, communicated internally and externally, for managing our business and evaluating our performance. We believe that providing non-GAAP measures affords investors a view of our operating results that may be more easily compared to the results of peer companies. In addition, compensation of our executives is based in part on the performance of our business based on these non-GAAP measures. However, non-GAAP information should not be construed as an alternative to GAAP information as the items excluded from the non-GAAP measures often have a material impact on PTC’s financial results and such items often recur. Management uses, and investors should consider, non-GAAP measures in conjunction with our GAAP results.

Non-GAAP revenue, non-GAAP operating expenses, non-GAAP operating margin, non-GAAP gross profit, non-GAAP gross margin, non-GAAP net income and non-GAAP EPS exclude the effect of the following items:

- Fair value of acquired deferred revenue is a purchase accounting adjustment recorded to reduce acquired deferred revenue to the fair value of the remaining obligation, so our GAAP revenue after an acquisition does not reflect the full amount of revenue that would have been reported if the acquired deferred revenue was not written down to fair value. We believe excluding these adjustments to revenue from these contracts (and associated costs in fair value adjustment to deferred services cost) is useful to investors as an additional means to assess revenue trends of our business.

- Stock-based compensation is a non-cash expense relating to stock-based awards issued to executive officers, employees and outside directors and to our employee stock purchase plan. We exclude this expense as it is a non-cash expense and we assess our internal operations excluding this expense and believe it facilitates comparisons to the performance of other companies in our industry.

- Amortization of acquired intangible assets is a non-cash expense that is impacted by the timing and magnitude of our acquisitions. We believe the assessment of our operations excluding these costs is relevant to our assessment of internal operations and comparisons to the performance of other companies in our industry.

- Acquisition-related charges included in general and administrative costs are direct costs of potential and completed acquisitions and expenses related to acquisition integration activities, including transaction fees, due diligence costs, severance and professional fees. In addition, subsequent adjustments to our initial estimated amount of contingent consideration associated with specific acquisitions are included within acquisition-related charges. These costs are not considered part of our normal operations as the occurrence and amount will vary depending on the timing and size of acquisitions.

- Restructuring charges include excess facility restructuring charges and severance costs resulting from reductions of personnel driven by modifications to our business strategy and not considered part of our normal operations. These costs may vary in size based on our restructuring plan.

- Non-operating credit facility refinancing costs are non-operating charges we record as a result of the refinancing of our credit facility. We assess our internal operations excluding these costs and believe it facilitates comparisons to the performance of other companies in our industry.

- Income tax adjustments include the tax impact of the items above and assumes that we are profitable on a non-GAAP basis in the U.S. and one foreign jurisdiction, and eliminates the effect of the valuation allowance recorded against our net deferred tax assets in those jurisdictions. Additionally, we exclude other material tax items that we view as non-ordinary course.

PTC also provides information on “free cash flow” and “adjusted free cash flow” to enable investors to assess our ability to generate cash without incurring additional external financings and to evaluate our performance against our announced long term goal of returning approximately 40% of our free cash flow to shareholders via stock repurchases. Free cash flow is net cash provided by (used in) operating activities less capital expenditures; adjusted free cash flow is free cash flow excluding restructuring payments and certain identified non-ordinary course payments. Free cash flow and adjusted free cash flow are not measures of cash available for discretionary expenditures.

Forward-Looking Statements

Statements in this press release that are not historic facts, including statements about our second quarter and full fiscal 2017 targets and other future financial and growth expectations, and anticipated tax rates, are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from those projected. These risks include: the macroeconomic and/or global manufacturing climates may not improve or may deteriorate; customers may not purchase our solutions when or at the rates we expect; our businesses, including our Internet of Things (IoT) business, may not expand and/or generate the revenue we expect; foreign currency exchange rates may vary from our expectations and thereby affect our reported revenue and expense; the mix of revenue between license & subscription solutions, support and professional services could be different than we expect, which could impact our EPS results; our customers may purchase more of our solutions as subscriptions than we expect, which would adversely affect near-term revenue, operating margins, and EPS; customers may not purchase subscriptions at the rate we expect, which could impact our ability to achieve expected subscription bookings and delay our exit from the subscription trough; sales of our solutions as subscriptions may not have the longer-term effect on revenue that we expect; our workforce realignment may not achieve the expense savings we expect and may adversely affect our operations; we may be unable to generate sufficient operating cash flow to return 40% of free cash flow to shareholders and other uses of cash or our credit facility limits could preclude share repurchases; and any repatriation of cash held outside the U.S., which constitutes a significant portion of our cash, could be subject to significant taxes. In addition, our assumptions concerning our future GAAP and non-GAAP effective income tax rates are based on estimates and other factors that could change, including the geographic mix of our revenue, expenses and profits and loans and cash repatriations from foreign subsidiaries. Other risks and uncertainties that could cause actual results to differ materially from those projected are detailed from time to time in reports we file with the Securities and Exchange Commission, including our most recent Annual Report on Form 10-K.

PTC and the PTC logo are trademarks or registered trademarks of PTC Inc. or its subsidiaries in the United States and in other countries.

About PTC (NASDAQ: PTC)

PTC has the most robust Internet of Things technology in the world. In 1986 we revolutionized digital 3D design, and in 1998 were first to market with Internet-based PLM. Now our leading IoT and AR platform and field-proven solutions bring together the physical and digital worlds to reinvent the way you create, operate, and service products. With PTC, global manufacturers and an ecosystem of partners and developers can capitalize on the promise of the IoT today and drive the future of innovation.